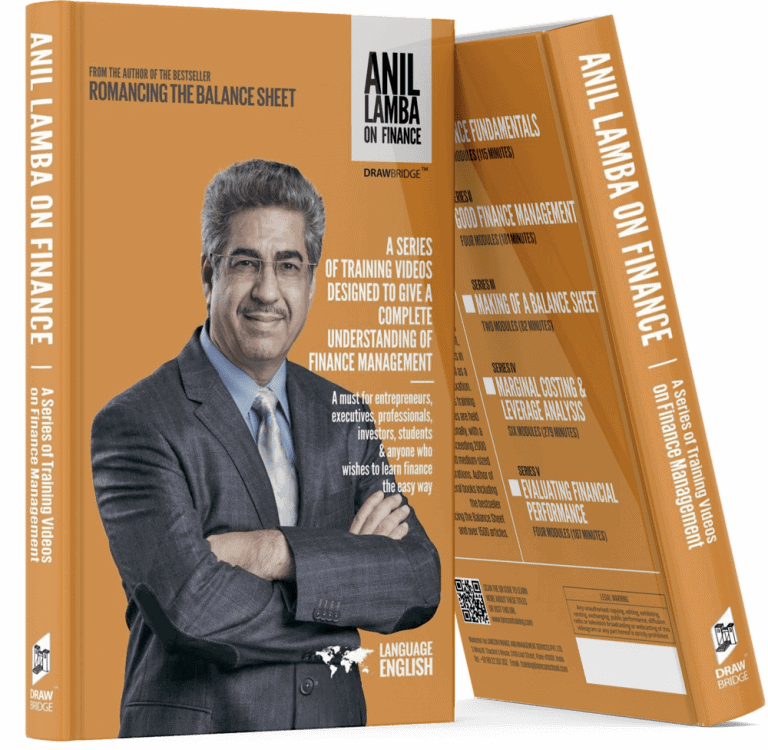

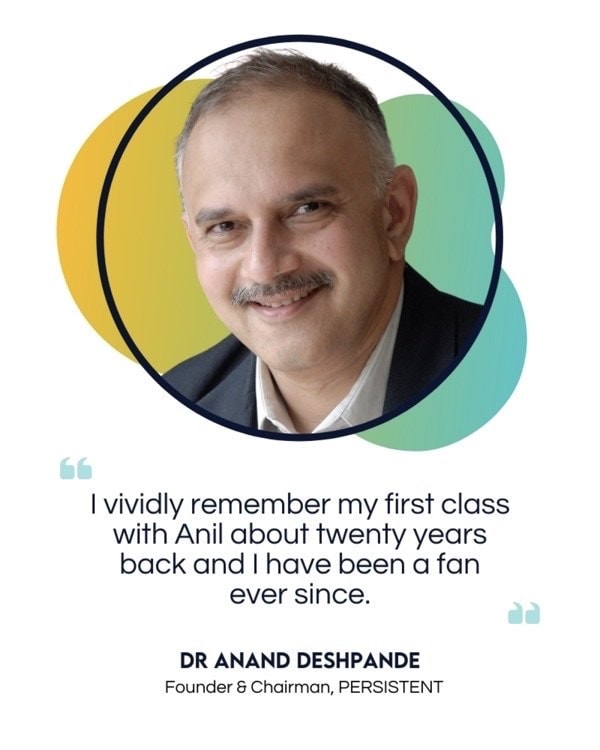

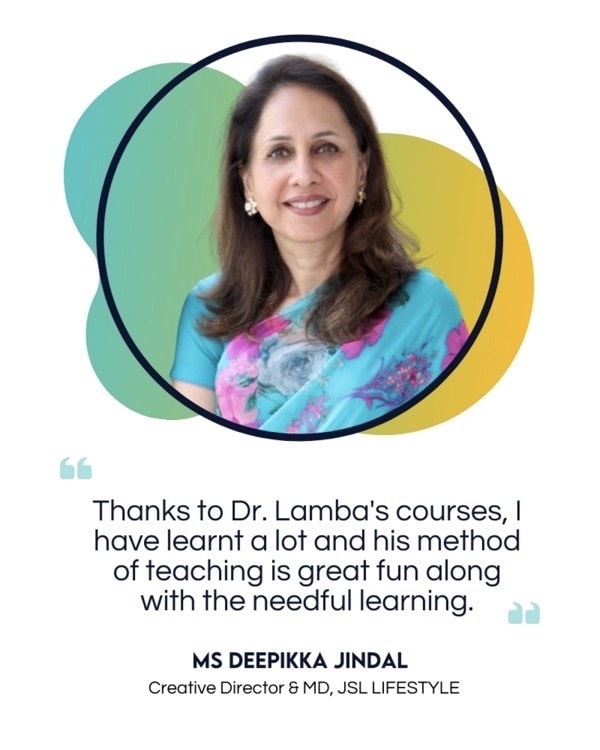

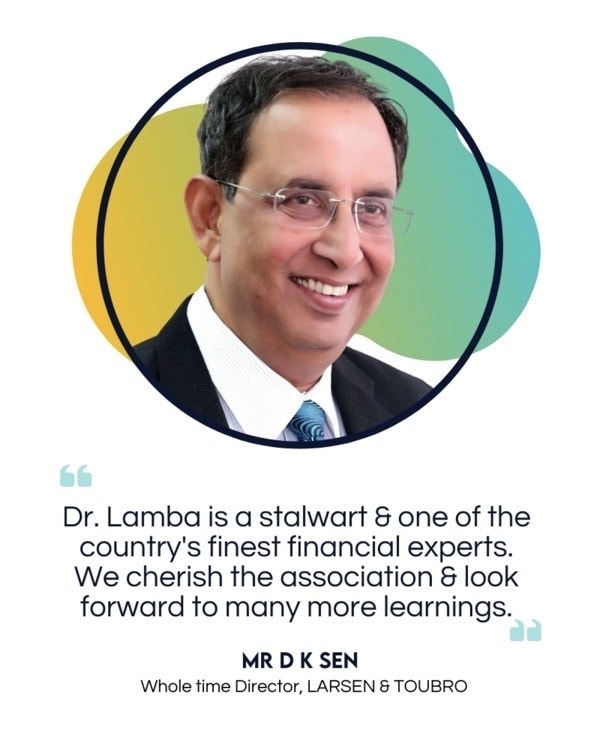

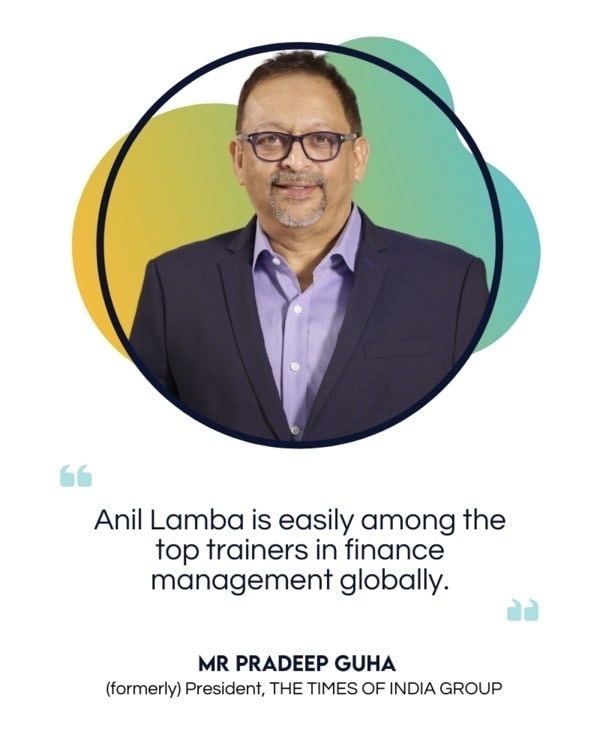

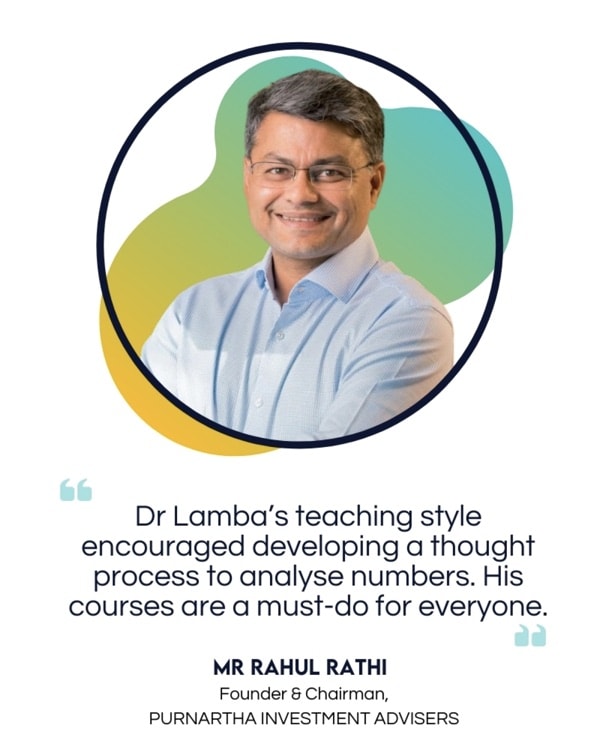

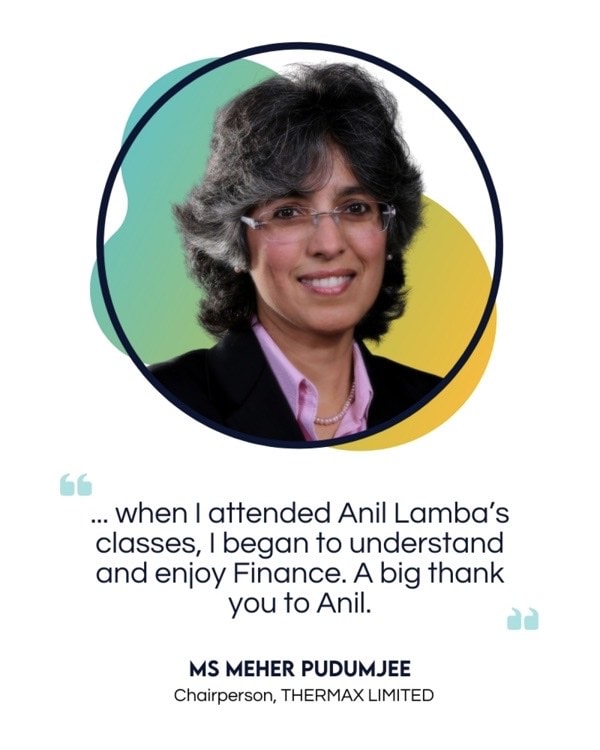

We are a leading provider of training programmes in finance management to corporations globally. Dr Anil Lamba has trained hundreds of thousands of executives, business owners, professionals and others from thousands of organizations in four continents.

Listen, read & watch